Insurance Claims in Connecticut: What Every Job Includes

Navigating a roof claim is a part-time job most homeowners don't have time for. We take it on: comprehensive damage documentation (the kind adjusters actually require), the paperwork packet, on-site representation when the adjuster comes out, supplement filing for items missed on the initial scope, and scope-of-loss disputes when needed. No upfront cost — for qualifying claims our work is paid through the insurance proceeds, and we're transparent about exactly how that math works.

- Damage documentation built around what adjusters look for

- On-site adjuster meeting representation

- Scope-of-loss review and supplement filing

- Denied-claim re-inspection support

- Honest read on whether your damage actually qualifies

- No upfront cost on qualifying covered claims

We know how stressful it feels to discover a leak right after a heavy Connecticut storm, which is why finding reliable Insurance Claim Assistance is so important. You might assume your homeowners policy will easily cover the repairs.

Recent 2024 National Association of Insurance Commissioners data shows that 40% of roof claims actually close with a $0 payout.

Our team will walk you through the exact steps to get approved.

This process does not have to be a headache.

Why Claim Advocacy Matters

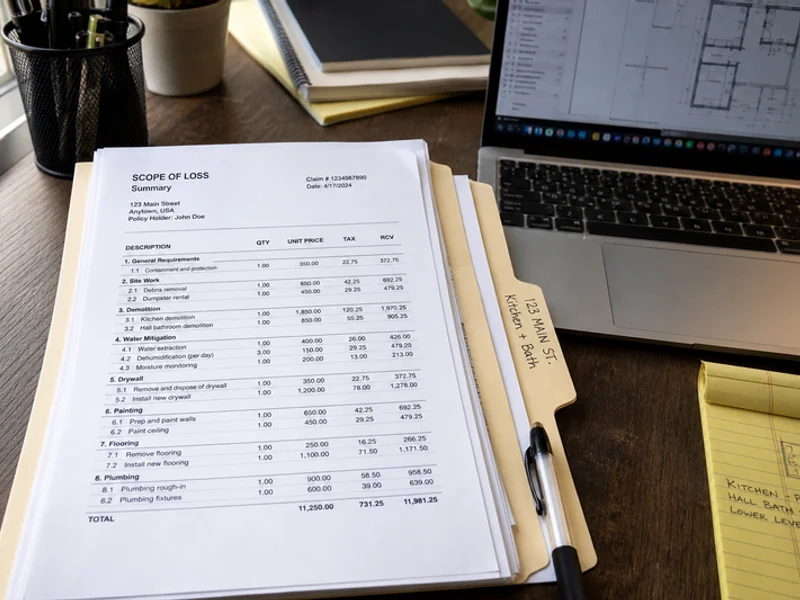

A roof claim has three documents that decide the outcome:

- The damage report (your evidence).

- The adjuster’s scope of loss (the insurer’s offer).

- Any supplements filed to add missed items.

We see most homeowners produce the damage report themselves with a few smartphone photos from the ground. You might let the adjuster’s scope of loss stand as the final number.

Our job is to put a professional roofing contractor in the meeting who has handled over 200 Connecticut claims. The result is that a meaningful share of legitimately covered damage gets missed during standard inspections.

We find that the adjuster’s exterior walk usually takes only 15 to 20 minutes. They are not climbing your steep slope to check the high valley shingles.

The Software and The Walk-Through

Our experts know exactly what the insurance company needs to see. Studies from the Office of Program Policy Analysis and Government Accountability show that having an advocate increases claim payouts by an average of 30 percent.

We ensure every required line item goes into Xactimate, which is the specific estimating software adjusters use. Many adjusters simply overlook bruising under the dirt on a heavily trafficked walk path.

Our presence completely changes the dynamic of that initial inspection. Connecticut code requires an ice and water shield on a full replacement, even if only a partial slope is damaged.

What’s Actually Covered

Local homeowner policies typically cover wind damage, hail damage, fallen debris damage, lightning strikes, and fire damage. We help you prove that sustained gusts above 50 mph lifted or tore your shingles.

Hail impact bruising on shingles from one-inch hail or larger qualifies for hail coverage. Our inspectors know exactly how to document this specific structural damage.

Most policies exclude wear-and-tear, age-related shingle failure, and gradual leaks not from a covered event. We explain the difference between sudden storm damage and long-term maintenance issues.

Understanding Your Building Codes

The 2022 Connecticut State Building Code strictly regulates how repairs happen. Our state requires ice and water barriers to extend from the lowest edges to a point at least 24 inches inside the exterior wall line.

If your existing roof lacks this barrier, a full replacement must include it to meet safety standards. We make sure your insurance estimate covers these mandatory code upgrades.

ACV vs. RCV Payments

Actual Cash Value versus Replacement Cost Value is another massive distinction. Our team always checks your policy declarations page to see which coverage you carry.

| Coverage Type | How It Pays | Financial Impact |

|---|---|---|

| Actual Cash Value (ACV) | Pays the depreciated value based on age. | A 15-year-old roof gets a significant payout cut. |

| Replacement Cost Value (RCV) | Pays the full current replacement amount. | Often arrives in two separate checks for full coverage. |

Many policies allow upgrading your coverage before a storm hits.

How the Work Gets Paid

For qualifying covered claims, the math typically looks very straightforward. We see that the insurance scope of loss might approve $14,000 in damage.

You pay your deductible, which is usually around $1,500, directly to your insurance company. Our crew does the work for the approved scope amount.

Payment happens in two distinct stages.

The Final Payment and Your Out-Of-Pocket

The first check covers the initial depreciated amount. We collect the second check for the recoverable depreciation after work completion.

Your net out-of-pocket expense is just your deductible. Our transparent process means you never see hidden fees.

Connecticut law actually requires insurers to pay the total amount of an agreed claim within 30 days of finalizing the settlement.

Average Costs and Honest Service

Average roof replacement costs in Connecticut range from $9,705 to $18,491. We tell you upfront if a claim lacks merit or will not qualify.

The exact price depends heavily on materials, like asphalt shingles versus a metal system. Our simple promise is that we will not push a claim that lacks evidence.

Honesty is the only way to do business.

The Next Step for Insurance Claim Assistance

Securing a fair settlement is completely possible with the right facts and representation. We hope this guide clears up the confusion around storm damage.

This process goes smoothly when you have the right support.

Our team is ready to inspect your property today. Give us a call to schedule your free roof assessment, and let us handle the heavy lifting of Insurance Claim Assistance for you.