The Six Steps to a Successful Roof Insurance Claim

We operate as a professional service team, and we see this scenario constantly across Connecticut after a severe storm passes.

Most property owners assume a prompt phone call to their agent guarantees a smooth repair process. Unfortunately, the path to a fair payout is rarely that simple. Data from the Connecticut Insurance Department in 2026 shows that companies are tightening their guidelines, making the ct roof insurance claim process more rigorous than ever.

Understanding how to file roof insurance claim connecticut documents properly can prevent a frustrating denial. Let’s walk through the exact sequence you need to follow. Our team will highlight critical deadlines, local code requirements, and the essential homeowner claim steps needed to protect your property.

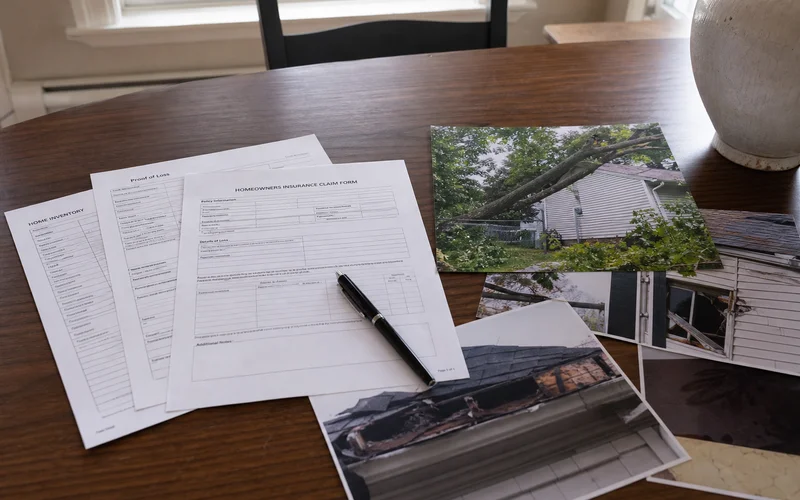

Step 1: Document the Damage Immediately

The moment you notice storm damage, your first priority is safety and documentation. Many Connecticut policies require you to report damage within a strict 30 to 90-day window. Missing this deadline is a common reason for a denied claim.

Our advice is to gather evidence before any cleanup begins.

- Photograph all visible damage from the ground level.

- Note the exact date and save local weather reports.

- Document interior ceiling stains or water marks immediately.

- Avoid making permanent repairs until an adjuster visits.

The photographs you take in the first 48 hours are incredibly valuable. Mold and structural decay begin fast, and adjusters often blame this secondary damage on homeowner negligence if a prompt report is missing.

Step 2: Get a Free Professional Inspection

Before you dial your insurance carrier, you need a professional assessment. A simple visual check from your driveway will not capture the full extent of the damage. You need concrete proof to get the adjuster’s attention.

We highly recommend scheduling a free post-storm inspection with a qualified local contractor.

This step provides two massive benefits:

- You avoid filing pointless claims. Marginal damage might not exceed your deductible, and filing roof claim connecticut paperwork with no payout still negatively impacts your risk profile.

- You get professional evidence. Experts use high-resolution tools to document hidden issues like wind-broken shingle seals.

Our team provides detailed inspections equipped with adjuster-grade photo reports. The inspection report is yours to keep, and using our repair services afterward is entirely optional.

Step 3: Notify Your Insurer

Once a professional confirms the damage, it is time to contact your insurance carrier. Connecticut property owners usually have a specific reporting window outlined in their policy declarations.

When making this initial call, keep the conversation brief and factual.

- Provide the precise date of the storm event.

- Describe the visible issues without guessing the cause.

- Mention your professional inspection report is ready.

- Ask for a clear outline of their expected timeline.

Our experience shows that volunteering repair estimates at this stage is a mistake. The adjuster’s job is to determine the financial scope during their physical visit. Simply open the claim and request a claim number.

Step 4: Schedule the Adjuster Inspection

Your carrier will assign an outside or desk adjuster to your case. They will typically schedule an on-site visit within one to three weeks. These representatives are often overworked, sometimes evaluating multiple properties in a single day.

You must prepare thoroughly for this meeting to ensure a fair assessment.

- Require a contractor presence. A roofer pointing out specific code violations catches items a rushed 20-minute walk misses.

- Organize your paperwork. Print your dates, weather logs, and professional reports.

- Stay available on site. Your ability to grant access and answer specific property history questions speeds up the process.

The adjuster will eventually produce a scope of loss document. This paperwork lists the approved repairs and the initial payout calculations.

Step 5: Review the Scope of Loss

You will receive the official scope of loss within a few weeks of the inspection. This document is the carrier’s opening offer, and it is almost never final. Most insurance companies use estimating software called Xactimate.

We review these documents daily and frequently find missing line items. Standard Xactimate scopes often apply bulk pricing that undervalues the actual labor required for spot repairs in our region.

You need to analyze the offer carefully.

| What to Verify | Why It Matters |

|---|---|

| Complete Damage Count | Are all affected slopes and elevations clearly listed? |

| Material Quality | Does the price reflect the actual brand of your existing shingles? |

| Labor Rates | Are the payouts realistic for the current Connecticut market? |

| Depreciation Applied | Is the deduction for age calculated correctly? |

If the estimate is too low, you have the right to file a supplement. A supplement is a formal request with documentation proving why additional funds are necessary. Industry data indicates that successful supplements can increase a final payout significantly, often covering missed local building codes.

Step 6: Schedule the Work

Once you and the carrier agree on the scope, the physical construction can begin. Payment structures for Replacement Cost Value (RCV) policies follow a very specific two-step process.

Our clients often ask how the money flows. Here is the standard timeline:

- The First Check: You receive the Actual Cash Value (ACV), which is the depreciated amount, right after approval.

- The Final Check: The carrier releases the remaining recoverable depreciation once you prove the work is fully complete.

You are responsible for paying your deductible directly to the roofing company. The contractor will then invoice the insurance provider for the remaining balance.

Common CT Carrier Quirks

Every state has unique regulations, and Connecticut is no exception. Understanding these local laws gives you a massive advantage during negotiations.

We always watch out for these specific regional patterns.

- The Connecticut Matching Law: Under C.G.S. § 38a-316e, if a partial repair creates a visible color or size mismatch, the insurer must replace adjacent items to ensure a reasonably uniform appearance.

- Strict Code Upgrades: The 2022 Connecticut State Building Code requires ice and water shield membranes to extend at least 24 inches inside the exterior wall line. Many generic scopes miss this costly requirement.

- Separate Deductibles: Coastal properties in Fairfield or New London counties frequently have distinct wind or hail deductibles that are percentage-based rather than a flat fee.

- Aggressive Depreciation: Carriers sometimes apply heavy depreciation schedules to roofs older than 15 years, greatly reducing that critical first check.

You must review your specific policy declarations page to see which of these factors apply to your situation.

What to Avoid

A stressed property owner is an easy target for bad advice. Making a rash decision immediately after a storm can ruin your chances of receiving full coverage. See also: Roof Insurance Claim Denied: What to Do Next.

Our team strongly advises against these three common errors.

- Signing an Assignment of Benefits (AOB) too early. Recent Connecticut legislation places heavy scrutiny on AOB contracts. Signing one transfers total control of your claim to a third party, leaving you with little power if disputes arise.

- Starting permanent repairs prematurely. Patching a leak with a tarp is fine, but replacing decking before an adjuster arrives destroys your evidence.

- Accepting the initial offer immediately. The first check is rarely sufficient to cover a complete, code-compliant replacement. You always have room to negotiate using a factual supplement.

How Our Advocacy Works

Managing a major property loss is a full-time job. Our dedicated insurance claim assistance service relieves that burden by handling the technical arguments for you.

This professional support applies specialized knowledge to every single step of the process.

- Compiling a complete damage documentation packet.

- Attending the on-site adjuster meeting to ensure accurate measurements.

- Filing detailed supplements when the initial scope misses vital components.

- Providing support for denied claim re-inspections.

We require no upfront costs for advocacy on qualifying covered claims. The compensation comes directly from the finalized insurance proceeds, alongside your standard deductible payment to the carrier.

Knowing how to file roof insurance claim connecticut documentation is the first step toward protecting your investment. Contact our office today to schedule your initial evaluation. The team will review your property and help you decide if moving forward makes financial sense.